Founder’s Note: I consider myself one of the luckiest guys in the business because of people like Sam Gatlin, Grant Hawkridge, and Jason Perz.

Sam, Grant, and Jason are the brains behind everything we do at TrendLabs. They prove it every day, especially on Saturday.

Here’s Jason with a great read about history, inflation, and energy. – JC

By Jason Perz

1968 was the worst possible time to retire.

Not because stocks crashed overnight or one catastrophic event.

Inflation showed up… and didn’t leave.

That’s the part most people get wrong. They think the big risk is a crash, a sudden drawdown – something obvious.

It’s not.

The real risk is slow. It grinds.

It sits there year after year, quietly destroying your purchasing power while your portfolio looks “fine” on the surface.

Inflation Is What Actually Destroys Portfolios

That’s exactly what happened starting in 1968.

According to William Bengen — the same guy who created the 4% rule — retirees in 1968 had it worse than those who retired at the peak in 1929.

Think about that.

The 1929 retiree went through the Great Depression… and still ended up better off in real terms than someone who retired in 1968.

Why?

From 1968 to the early 1980s, the cost of living nearly tripled. Inflation peaked at 13.5%. And that one force — more than any bear market — destroyed portfolios.

When inflation rises, your withdrawals rise with it. And once those withdrawals increase, they don’t come back down.

You’re pulling more out of your portfolio every year… while the real value of your assets is getting crushed.

That’s how portfolios go to zero – not in a crash, but over time.

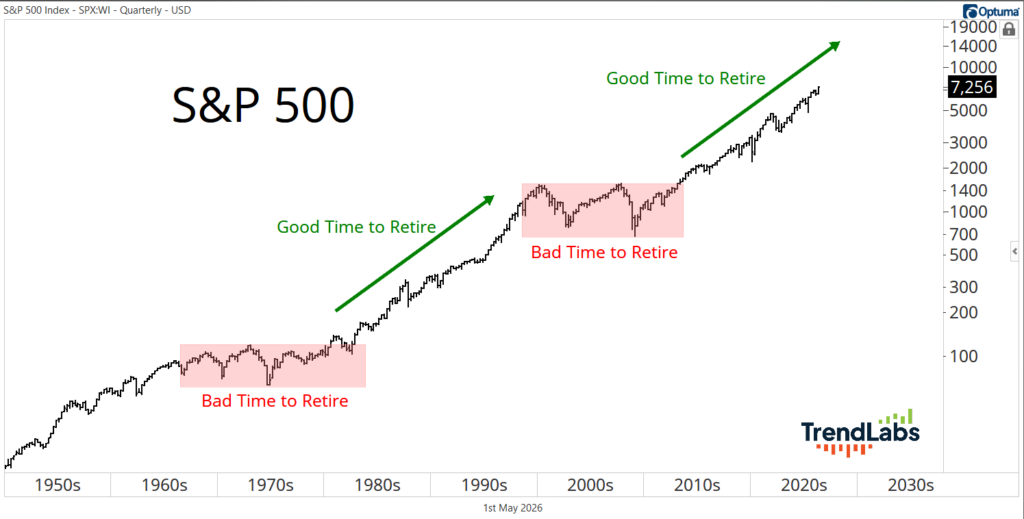

Now look at the chart:

You can clearly see it.

The late ’60s into the early ’80s was a brutal environment. Sideways markets, high inflation: a terrible time to retire.

Then it happened again.

From 2000 to 2011, another inflationary stretch. Not as extreme, but still enough to create a lost decade for stocks while commodities and real assets outperformed.

These aren’t random periods.

They’re inflation regimes.

This Is Why Positioning Matters Right Now

And today? We’re setting up for the next one.

Gold has already broken out to new highs. Copper is confirming. Oil is starting to move.

That’s the cycle.

Gold → Copper → Oil

And when that sequence plays out, it tells you one thing: Inflation is not going away.

So, are you positioned for it? Because most portfolios are not.

Traditional allocations — heavy stocks and long-duration bonds — get exposed in this environment.

Bonds get crushed as yields rise. Dollars get crushed through debasement. Stocks struggle to keep up with rising costs and tightening conditions.

There’s a better way.

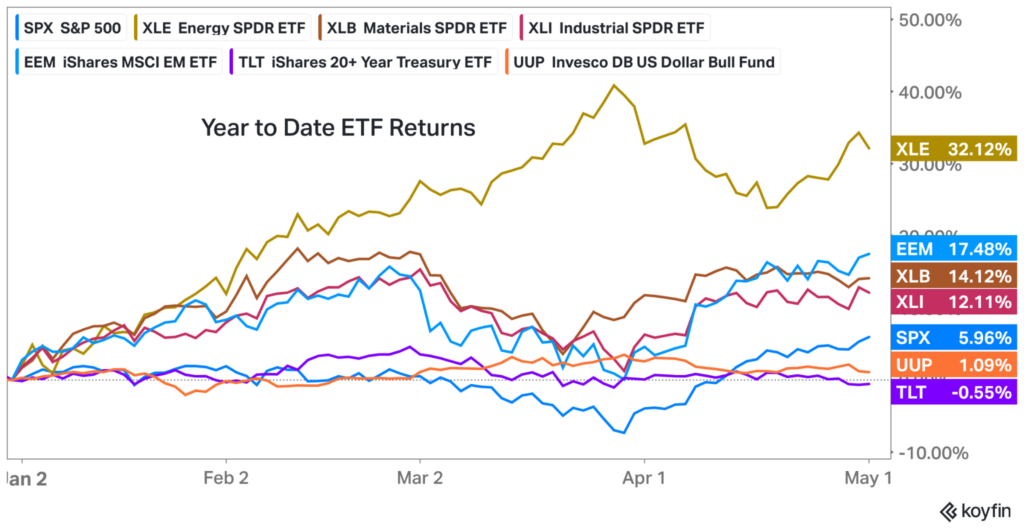

See what’s working in 2026:

If inflation is the problem, your portfolio needs assets that benefit from it.

Energy. Metals.International equities. Real assets tied to the global economy.

These are the areas that outperform when inflation trends higher.

This isn’t theory. It’s history.

And it’s exactly how we’re positioned.

We’re not guessing. We’re following the playbook that’s worked in every inflationary cycle before this.

Investing isn’t about chasing returns.It’s about protecting your purchasing power first — and growing it second.

The next inflation regime isn’t coming.It’s already starting.

Don’t wait until it’s obvious.

By then, the move is already gone.

Save the bees,

Jason Perz

Senior Analyst, TrendLabs