The SpaceX IPO is finally here.

Depending on where it ultimately opens, we’re talking about a company worth somewhere between $2 trillion and $3 trillion.

One company.

At the upper end of that range, we’re approaching 10% of annual U.S. GDP. Think about that for a second. One stock. One listing. One afternoon.

And they’re opening it on a Friday in the middle of the summer.

Really?

After more than two decades of watching markets, I find that part almost as fascinating as the company itself.

Because regardless of what anyone thinks about SpaceX, this is a market structure event as much as it is a company event.

And I don’t think enough people appreciate that.

The Biggest IPO Ever Isn’t Supposed To Be Easy

The first thing that jumped out at me wasn’t the valuation.

It was the calendar.

The largest IPO in history is scheduled to begin trading on a summer Friday afternoon.

That’s an extraordinary amount of capital trying to find a home in a relatively quiet market environment.

To be fair, the exchanges deserve some credit. Nasdaq reportedly adjusted procedures and listing requirements to help facilitate a faster launch process.

That’s probably necessary when you’re dealing with an offering of this magnitude.

They want this to go well.

They have every incentive in the world for it to go well.

If Nasdaq handles this smoothly, it reinforces its position as the preferred destination for the world’s most important technology companies.

If it doesn’t, every future mega-listing has another option waiting for them downtown at the New York Stock Exchange.

The stakes are enormous.

But history tells us that enormous IPOs don’t always cooperate.

The Facebook launch in 2012 was a complete disaster. Technical issues delayed executions and created confusion throughout the market. Investors were furious. Brokers were scrambling. Everyone was frustrated..

And the Facebook IPO was tiny compared to this.

I’ve been doing this for 23 years. I’ve seen enough market events to know that people dramatically underestimate operational risk when something unprecedented happens.

I’m not saying this as a prediction, but more so as a warning: There’s a real possibility this thing doesn’t even start trading today.

I hope it does. I hope it’s smooth.

I hope the market absorbs it effortlessly and everyone moves on with their lives.

Historically, that’s not usually how these stories go.

History Is Not Exactly Encouraging

Whenever investors encounter something this large, they immediately start searching for comparisons.

I’ve been doing the same thing.

In 1901, J.P. Morgan assembled U.S. Steel into the largest corporation the world had ever seen.

It represented a massive percentage of the economy and captured the imagination of investors everywhere.

Shortly afterward, the Dow was cut in half:

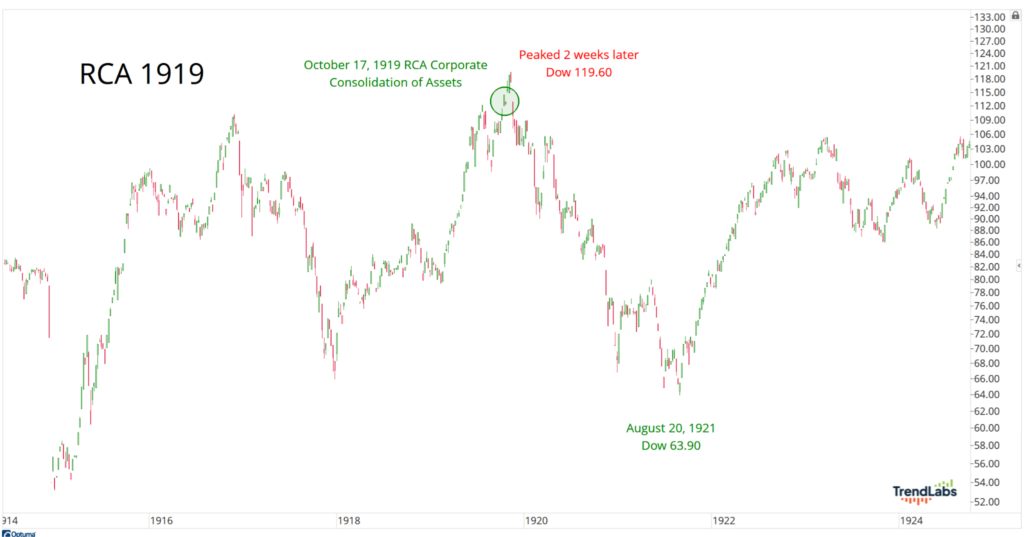

In 1919, RCA became the public vehicle for the radio revolution. Investors weren’t buying a company. They were buying the future.

Just two weeks later, the Dow peaked and quickly got cut in half:

In 1956, Ford went public in one of the most anticipated offerings in American history. Much like SpaceX today, early investors and founding stakeholders were creating liquidity in a company that had already become iconic.

Ford peaked on its first day. The broader market entered a bear market not long after.

More recently, the list isn’t much friendlier.

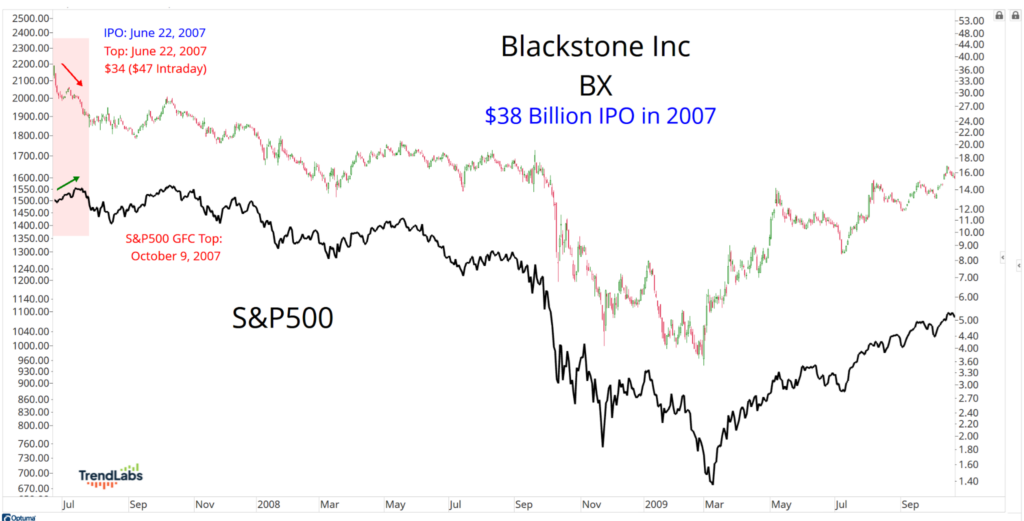

Blackstone in 2007 peaked on its first day and crashed, losing 90% of its value and officially kickstarting the Great Financial Crisis:

Facebook in 2012. Same thing. Peaked on its first day and immediately crashed 60%.

Coinbase in 2021. Disaster. Peaked on its first day and fell over 90%. It also marked an important high for the price of Bitcoin:

Uber in 2019 peaked the following month and crashed.

Rivian in 2021 is the biggest recent IPO we’ve seen in America during modern times, $80 Billion in market capitalization.

It peaked a week after going public and immediately lost over 95% of its value.

Again and again, massive offerings arrived amid tremendous excitement and often marked important peaks, either in the stock itself or in the surrounding market environment.

That doesn’t mean SpaceX must follow the same script.

History doesn’t repeat perfectly. But it rhymes often enough that I think it’s worth paying attention.

What’s interesting this time is that we’re already seeing the opposite side of the argument.

Barron’s is questioning the valuation:

Plenty of commentators are arguing that it’s too expensive.

Others are arguing that it’s already too large:

As students of sentiment, we have to acknowledge that.

Universal optimism is dangerous. Universal skepticism can be useful.

And that’s why I continue to think the best historical comparison isn’t railroads or automobiles.

It’s the Dutch East India Company.

The Dutch East India Company represented a new frontier.

It opened trade routes that previously didn’t exist. It expanded the economic map of the world.

Yes, it eventually became part of a speculative bubble.

But before that? It created wealth for generations. For centuries.

When I think about exploring the oceans versus exploring space, that comparison makes more sense to me than most of the others.

Railroads eventually reach the coast.

Space doesn’t.

What Does It Mean for Us?

The other day I was explaining the IPO to my wife. I told her it was the biggest IPO ever, by a long shot.

I told her the valuation could be trillions of dollars. I told her the whole financial world would be watching.

Her response was simple.

“OK. What does it mean for us?”

Honestly, that’s the best question I’ve heard throughout this entire process.

Because at the end of the day, I don’t get paid for having opinions about valuations.

I get paid for managing risk. I get paid for identifying trends. I get paid for recognizing when buyers or sellers are in control.

For me, everything starts with the anchored VWAP from the IPO. This is what I like to call the “Genesis Line.”

It’s the volume weighted average price of the stock from the second it opens.

Here’s how I’ll be using it: If price remains below the Genesis Line, then sellers are in control.

That’s exactly what happened in many of the major IPOs we’ve discussed. Initial excitement fades, supply overwhelms demand, and the stock enters a long period of digestion.

That process can take quarters.

Sometimes years.

My base case is that SpaceX probably pops initially, and then it gets stuck below its Genesis Line.

Maybe it peaks on day one. Maybe it spends months consolidating.

But my guess is that it frustrates everyone before eventually emerging and becoming a $10 trillion company years from now.

That’s actually the path that would make the most sense to me.

And there are a few ways to play it, if you even want to. Remember, you don’t need to trade this stock. There are thousands more to choose from.

For me, the only way to be long this week or next week, is if prices are above their anchored VWAP from the initial print – the Genesis Line.

If it’s below that, then we can’t touch it from the long side. It’ll probably even be a good short.

My suspicion is that it’s going to take some time to digest all of this supply. It could take months, or even quarters. Maybe longer.

But the point remains the same. We want to only be long above the genesis line. Below that and it’s a no go.

Now, could it open at a massive valuation and continue climbing immediately?

Of course.

Anything is possible.

I’ve learned not to underestimate a market that’s willing to pay almost any price for the assets it wants.

But if I’m going to own it, I need evidence.

I need proof that buyers remain in control.

And for me, that proof begins with one simple question:

Is SpaceX above or below the Genesis line?

Everything else is just noise.

Stay sharp,

JC Parets, CMT

Founder, TrendLabs