Are you surprised stocks aren’t down more?

Because if you’re just following the headlines, they’ll tell you things are breaking down everywhere. Bear market. Risk off. Get defensive.

But when you actually look under the hood, it’s a different story.

New lows on the New York Stock Exchange (NYSE) aren’t expanding. They’re shrinking.

Each week, fewer stocks are participating in the downside, even as the indexes themselves flirt with fresh lows.

That’s not what real deterioration looks

If stocks are “breaking down,” where are the sellers?

One possible answer is that they’re already gone.

Investors have spent weeks, maybe months, preparing for chaos. They’ve hedged, de-risked, raised cash, and in many cases already sold what they wanted to sell.

If that’s true, then what we’re left with is a market where the pressure isn’t coming from new sellers.

It’s coming from a lack of them.

And that changes everything.

Who’s Left To Sell?

Charlie McElligott of Nomura said it best this week: “Stocks refuse to crash because we’re too hedged for chaos.”

That’s not a throwaway line. That’s positioning.

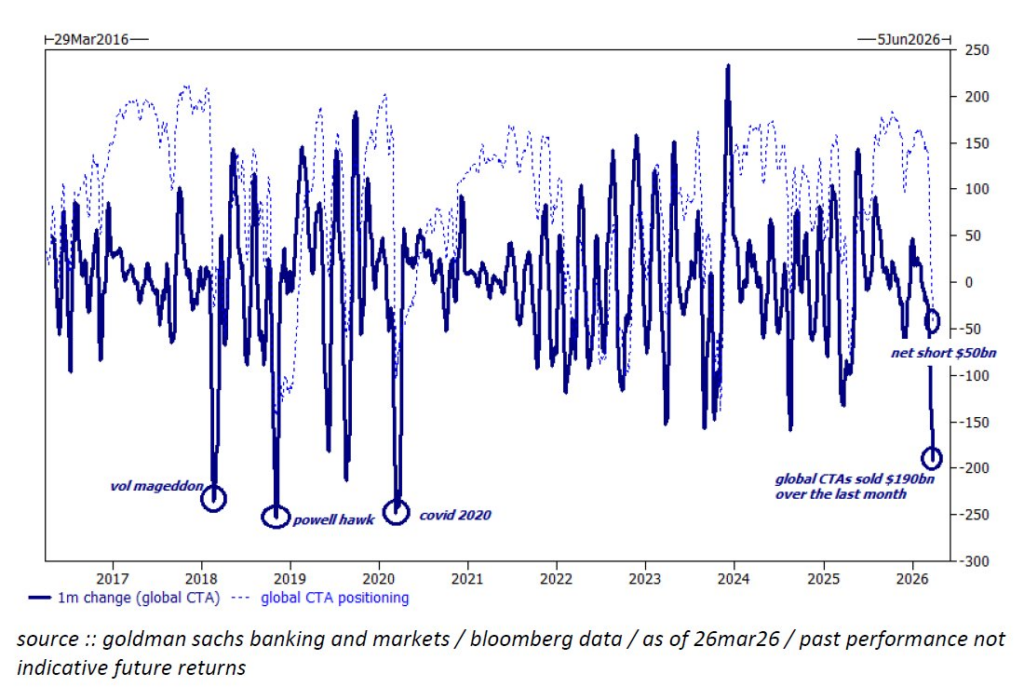

Commodity trading advisor (CTA) trend followers have been dumping risk aggressively.

Goldman Sachs estimates they sold about $190 billion in equities this month and are now net short roughly $50 billion globally:

This isn’t discretionary selling. These are systematic players doing exactly what they’re programmed to do as trends weaken.

But here’s the part that matters.

When this group gets this short, historically it hasn’t marked the start of sustained downside. It’s been much closer to the end of it.

Because once they’re short, the next move is buying.

Goldman’s Brian Garrett is already pointing in that direction. His team expects CTAs to be buyers over the next month in basically any scenario.

Think about what that means.

If the marginal seller has already sold, and is now mechanically turning into a buyer, the pressure flips.

If that shift is already starting, it would help explain what we’re seeing beneath the surface.

Stocks that refuse to go down.

The Tape Isn’t Confirming It

The indexes made new lows yesterday. The S&P 500 did it. The Nasdaq-100 did it. Even some of the recent leaders finally saw a little pressure.

That’s what the headlines focused on.

But underneath the surface, the data told a completely different story.

Fewer stocks on the NYSE hit new 52-week lows than last week. And last week had fewer than the week before.

That’s the opposite of what you see in real breakdowns. You want expansion in new lows. We’re getting contraction.

Now look at participation.

The percentage of stocks above their 200-day moving average rose. Same thing for the 50-day. Even shorter term, the percentage above the 20-day surged and is nowhere near the washed-out levels from just two weeks ago.

So while indexes are probing lower, more stocks are actually holding up or improving.

That’s not distribution. That’s absorption.

Then there’s breadth.

The cumulative advance-decline lines for both the NYSE and the S&P 500 actually moved higher. Not by much. But they didn’t fall. On a day when indexes made new lows.

Think about that for a second.

If you want a group to watch, look at financials.

We don’t get sustained bull markets without them, and they were up over 1% yesterday.

Right off support at that 61.8% retracement from last year’s rally:

When financials are rising while the indexes are making new lows, I pay attention.

When everyone is telling you stocks are falling apart, and the data says otherwise, I pay even closer attention.

Because if everyone is positioned for chaos, and the market still can’t go down, that’s not weakness.

That’s something else.

So is the market actually too hedged for chaos?

The math checks out.

Stay sharp,

JC Parets, CMT

Founder, TrendLabs