Before we get started, a quick reminder:

The Federal Reserve begins a two-day policy meeting this week, the first one under new Chair Kevin Warsh.

And yes, his name is Kevin.

Which means we should probably prepare ourselves for years of “Home Alone” jokes.

Every time markets get volatile, somebody is going to post a picture of Mrs. McCallister screaming, “KEVIN!”

Honestly, it might be funny the first hundred times.

After that, we’ll see.

Anyway…

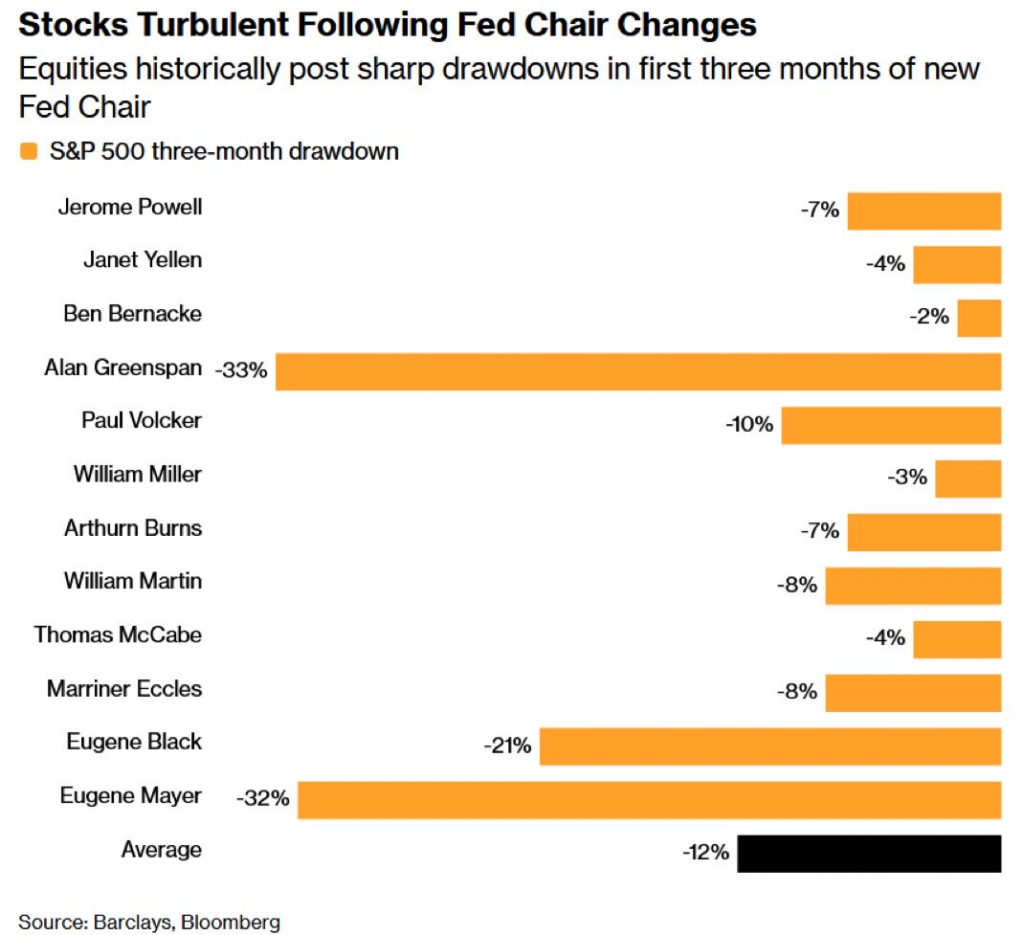

Ever since Warsh was sworn in, a chart has been making the rounds.

It shows how poorly the stock market has performed during the first few months after a new Fed chair takes over.

The implication is obvious: “Be careful. The market is about to test the new guy.”

Here’s the problem: The market doesn’t really care who the new Fed chair is.

At least not the way people think.

The stock market is constantly looking ahead. Investors are always trying to figure out what the world will look like tomorrow, next month, and next year.

By the time a new chair actually gets the job, investors have already spent months, and often years, thinking about all the possible outcomes.

That’s why I’m skeptical whenever I see headlines suggesting stocks should fall simply because somebody new moved into the chair’s office at the Fed.

The evidence isn’t nearly as convincing as the headlines make it sound.

And if your study depends heavily on a couple of guys named Eugene running the Federal Reserve during the Great Depression, that’s probably important context.

The Eugene Effect

The data comes from a study compiled by Barclays.

At first glance, it looks scary.

Since the 1930s, stocks have tended to experience larger-than-normal pullbacks during the first three months after a new Fed chairman takes over.

In fact, the average decline in this table has been roughly 12%, which is certainly enough to grab investors’ attention:

Sounds ominous. But maybe there’s another explanation.

Maybe markets are just doing what markets normally do.

Stocks experience pullbacks all the time.

That’s not unusual. That’s normal.

If you’ve been around markets long enough, you learn that investors love attaching stories to ordinary market behavior.

A 5% decline feels incredibly important when there’s a new Fed chair.

The same 5% decline during any other random quarter barely gets anyone’s attention.

That’s the problem with studies like this.

They tell us what happened.

They don’t necessarily tell us why.

And when you dig into the numbers, a surprising amount of the weakness comes from a very specific period in history.

During the Great Depression, two different Fed chairs happened to be named Eugene.

That’s not a joke.

Eugene Meyer became chair in September 1930 as the Depression was getting worse.

Eugene Black took over in May 1933 during one of the most chaotic periods in American financial history.

Those were extraordinary circumstances.

Banks were failing.

The economy was collapsing.

Unemployment was soaring.

If much of the bearish evidence comes from events that occurred while two guys named Eugene were rotating through the Federal Reserve during the Great Depression, it’s fair to ask how relevant those results really are today.

The chart becomes a lot less dramatic when you focus on the modern era.

Ben Bernanke inherited a housing bubble that eventually turned into the Global Financial Crisis.

Jerome Powell inherited a pandemic, supply-chain disruptions, trillions of dollars in stimulus, and the highest inflation in forty years.

Those were extraordinary environments.

Yet the market drawdowns following modern Fed leadership changes generally look a lot like the normal drawdowns we see all the time.

In other words, there doesn’t appear to be anything particularly special about a new Fed chair.

Watch Fed Funds Futures, Not Headlines

If investors were truly testing Kevin Warsh, where would we see it?

Not in a random 3% or 5% move in the stock market.

We’d see it in interest rate expectations.

We’d see it in the federal funds rate futures market.

For anyone unfamiliar, fed funds futures are simply a market where traders place bets on what they think the Fed will do with interest rates.

The Fed holds eight scheduled meetings each year. If investors believe a new chair is going to dramatically change policy, this is where those expectations show up first.

If investors suddenly thought Warsh was going to be much more aggressive than Powell, or much more willing to cut rates, we’d see it immediately reflected in futures pricing.

And right now?

We’re not seeing that at all.

The futures market is pricing in no change at Warsh’s first meeting this week.

It’s pricing in no change at the July meeting.

And it’s pricing in no change at the September meeting.

Three meetings.

Three expected holds.

None.

Despite all the headlines debating whether Warsh will be more hawkish or more dovish than Powell, investors aren’t pricing some dramatic shift in policy.

That’s important.

Because fed funds futures represent what investors actually believe.

Headlines represent what journalists think people are talking about.

Those are not the same thing.

Stocks don’t go up or down.

They go up and down.

That’s what they do.

A pullback by itself doesn’t tell us much.

But if interest rate expectations begin changing materially, then we can start talking about whether investors are embracing or rejecting the new chair.

Until then, what we’re seeing looks a lot less like a test of Kevin Warsh and a lot more like ordinary market behavior being dressed up as something extraordinary.

And if stocks happen to be down a few percent next week, don’t worry.

Someone on television will blame Kevin.

Stay sharp,

JC Parets, CMT

Founder, TrendLabs