For years I’ve been saying that the 60/40 portfolio is really 100.

People hear “60/40” and think about a balanced mutual fund or some financial advisor allocating 60% to stocks and 40% to bonds.

But that’s not what I’m talking about.

I’m talking about a philosophy. A religion.

The belief that stocks and bonds are fundamentally different animals.

Stocks provide “growth.” Bonds provide “protection.” When one zags, the other one zigs. When stocks get into trouble, bonds come to the rescue.

That assumption became embedded into the foundation of modern portfolio construction. And we’re not talking about a niche corner of finance.

Global asset managers oversee approximately $140 trillion. Global stock market capitalization currently sits near $150 trillion. Global bonds outstanding total about $145 trillion.

Depending on how you define it, there’s more than $400 trillion of investable wealth on earth.

My estimate is that somewhere around $100 trillion is directly or indirectly influenced by this stock/bond diversification framework.

Not because everyone owns a literal 60/40 portfolio.

Because public pensions, sovereign wealth funds, teacher retirement systems, insurance companies, corporate retirement plans, target-date funds, endowments, foundations, and private wealth managers all grew up under the same doctrine.

State and local public pensions alone manage roughly $6.8 trillion.

The largest pension funds in the world control trillions more. Just seven of the largest retirement funds on the planet oversee more than $6 trillion by themselves.

Meanwhile, the largest corporate pension plans at companies like IBM (IBM), Boeing (BA), Verizon (VZ), AT&T (T), Ford (F), General Motors (GM), Exxon Mobil (XOM), and General Electric (GE) still collectively represent enormous pools of capital built on these same assumptions.

Many of these institutions don’t even run classic 60/40 portfolios anymore. They’ve added private equity, infrastructure, private credit, real estate, hedge funds, and all sorts of alternatives.

But the philosophy remains the same: “Growth assets + Defensive assets = Diversification.”

The problem is that correlations don’t care what your investment committee believes.

The Relationship Changed

The biggest story in markets isn’t AI.

It’s not tariffs, it’s not geopolitics, and it’s not the Fed.

The biggest story is that one of the most important relationships in all of finance has been changing right in front of our eyes.

For decades, investors became accustomed to a world where bonds could cushion equity declines. That relationship became so accepted that it stopped being questioned.

Then 2022 happened. Stocks got crushed. Bonds got crushed.

The traditional diversified portfolio suffered the worst year in its history. Most investors viewed that as an anomaly.

I don’t.

I think it was a warning.

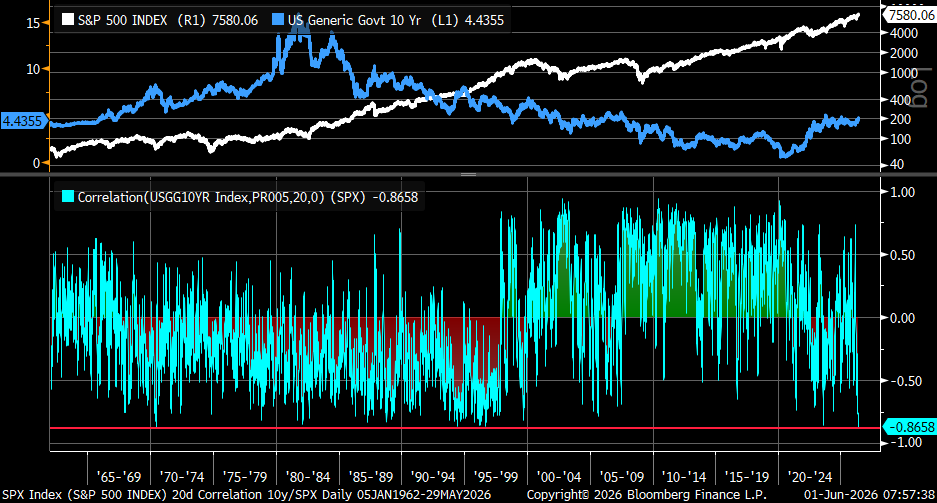

Recently, Kevin Gordon over at Schwab highlighted a remarkable statistic.

The rolling 20-day correlation between changes in the 10-year Treasury yield and the S&P 500 fell to its most negative reading on record:

This isn’t a chart that starts during the financial crisis. It doesn’t start in the tech bubble. It goes all the way back to the 1960s.

And today we’re seeing an extreme never witnessed before.

Think about what that means.

The market is telling us that interest rates matter more than most investors appreciate.

Stocks have done just fine with interest rates moving sideways. They’ve even handled moderately higher rates better than many expected.

But what happens if the bond market becomes the story?

What happens if Treasury yields continue to move higher for reasons that have nothing to do with economic growth?

That’s where things get interesting.

Because the assumption that bonds are always there to save you has already been challenged.

The next phase may be proving they can become the source of the problem.

The Next Panic Might Already Be Starting

Every bear market has its thing.

In 2000, it was technology. In 2008, it was housing and credit. In 2020, it was the global shutdown.

The next one?

My guess is bonds.

Not because bonds are going away. They’re not.

Not because rates are about to explode tomorrow. Maybe they won’t.

But because the entire investment industry remains built around assumptions that were developed during a very specific interest-rate regime that no longer exists.

There are risk-parity models, institutional asset-allocation models, pension models, volatility-targeting models, and countless algorithms that depend on relationships behaving a certain way.

Some of those relationships have already broken. Others are starting to crack.

Most people aren’t talking about it yet because stocks continue making new highs. As long as portfolios are working, nobody asks many questions.

But, eventually, they will.

At some point, the conversation will shift from market concentration. It will shift from AI. It will shift from whatever headline happens to be dominating financial television that day.

People will begin asking why “diversified portfolios” aren’t diversifying.

Why stocks and bonds aren’t behaving the way they’re supposed to.

Why trillions of dollars built around decades-old assumptions suddenly feel vulnerable.

That’s when everyone will notice the storm.

The market notices it first. It always does.

Judging by what the bond market has been telling us, I don’t think this story is ending…

It’s just getting started.

Stay sharp,

JC Parets, CMT

Founder, TrendLabs