Founder’s Note: Grant Hawkridge joined us up here in the Northern Hemisphere last week for some good times, some great conversions, and some fantastic breakthroughs.

That’s what happens when you get out and get together with your people.

Here’s Grant with some reflections on another productive visit to the States… – JC

By Grant Hawkridge

G’day, Grant here again.

Everyone keeps talking about opportunity right now, whether that’s the AI boom, the SpaceX IPO, or some other trillion-dollar theme.

Every second headline feels like someone trying to convince you that you’re either early to the future or about to miss it completely.

After spending the last two weeks in the U.S. sitting in a room full of traders debating markets, systems, and processes, I kept coming back to the same thought…

Most investors completely misunderstand what opportunity actually looks like.

One of the biggest opportunities I got from the trip had nothing to do with AI or IPOs.

It came from getting to spend a week face-to-face with JC.

Most of the year we’re spread all over the place, in different countries and across time zones.

We talk all the time, but it’s never quite the same as sitting in the same room working through ideas together.

That’s usually when we’re at our best.

Somebody throws out an idea. Somebody else challenges it. Another person looks at it from a completely different angle.

Before long, you’re looking at the same problem in ways you never would have on your own.

One of the things we spent a lot of time discussing was an idea JC has been trying to solve for years.

We’ve seen plenty of examples where a stock gets knocked down, spends months stuck below a level, then finally breaks back above it and takes off.

JC calls these “volume pockets,” areas where very little trading took place, which can sometimes act like a vacuum once price gets back into them.

We’ve seen these setups work over and over again in the market.

The problem wasn’t understanding them. The problem was figuring out how to consistently identify them before they became obvious to everyone else.

So we spent the week drawing it out, testing different ideas, trying to figure out how to turn something we could see with our eyes into something a computer could identify automatically.

The funny part is that by Friday afternoon it felt like things finally started clicking.

I’d been up at 5 am in Nashville working on the problem and building out a way to quantify it.

Later that afternoon, after hours of discussion and bouncing ideas around the room, it turned out we’d basically arrived at the same answer.

I always find those moments interesting. When smart people attack the same problem independently and end up in roughly the same place, you usually know you’re onto something.

That’s one of the reasons I always look forward to these trips.

You can spend months working on something remotely. Then you get everybody in the same room for a few days and suddenly things start moving much faster.

That’s what opportunity looks like to me.

It’s not sitting around waiting for the next hot story. It’s getting the chance to work with smart people, challenge ideas, test theories, and leave with a better process than you had when you arrived.

That’s why I find the reaction around the SpaceX IPO so fascinating right now.

Most investors already see it as the opportunity of the decade before the stock has even had a chance to properly trade.

And I understand why.

You’re talking about one of the most dominant private companies in the world.

It’s rockets and satellites, Starlink and Mars. It almost feels bigger than just another stock market listing.

For a lot of investors, owning SpaceX feels like owning a piece of the future itself.

Maybe eventually it does become an incredible opportunity.

But from the way I look at markets, I honestly don’t care yet.

It’s not because I think the company’s bad, or that I think the story’s wrong.

I just don’t have any price action. There’s no trend. There are no important levels.

There’s no real way to define risk.

At this stage, all I really have is a story. And great stories don’t necessarily make great opportunities.

The funny thing about the best opportunities is that they usually don’t feel obvious at the time. If they did, everyone would already be positioned for them.

That’s one of the reasons I spend so much time looking at data that sits away from the headlines.

Most investors spend their time focused on the stories everyone is talking about.

Sometimes the biggest clues come from the places nobody is paying attention to.

What the Market Isn’t Worried About

One of the things I’ve been paying close attention to recently is whether there’s any evidence of financial stress starting to build beneath the surface of the market.

That sounds boring. I get it.

But this is the type of data that actually helps you understand whether the market is under real pressure, or whether people are just stressed about the stories in front of them.

There’s a difference.

If you turn on the news every day, you’d think investors have a new reason to panic every week. It’s all tariffs and interest rates, government debt and recession forecasts. The list never seems to end.

But when you start digging into the actual data, a different picture starts to emerge.

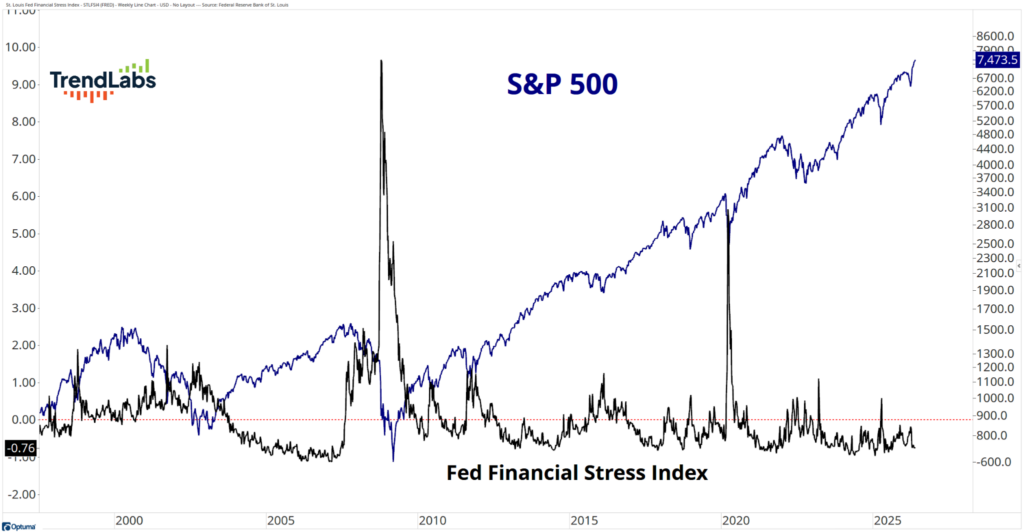

The first chart is the Fed Financial Stress Index:

Think of it as a pressure gauge for the financial system. Banks, lending markets, funding markets, and credit conditions all feed into it.

Historically, this index spikes when something is breaking, like during the Great Financial Crisis or the COVID crash.

Major periods of financial stress all show up very clearly.

Right now, it’s sitting below zero.

In plain English, the financial system isn’t behaving like it’s under pressure.

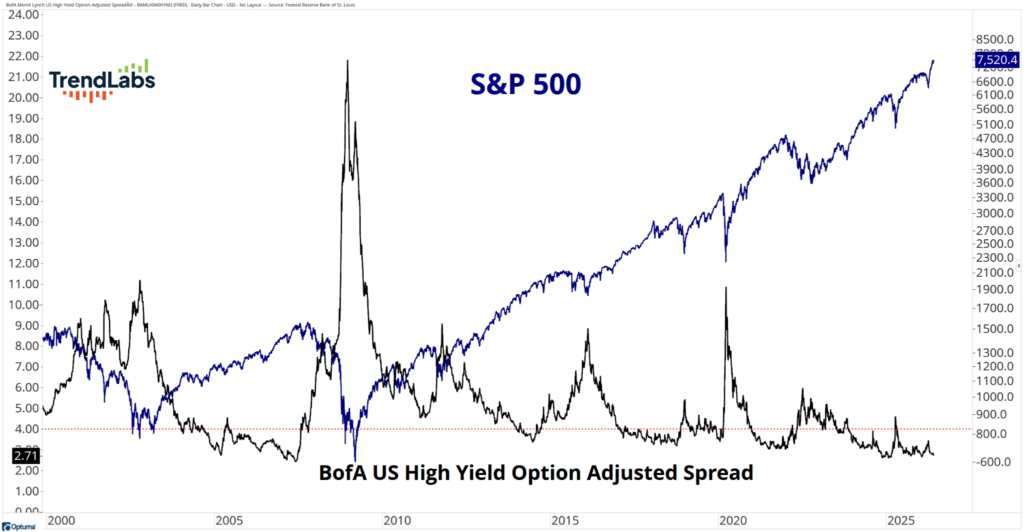

The second chart tells a similar story:

High-yield credit spreads measure the extra interest investors demand for lending money to riskier companies.

When investors become worried about defaults, recession, or economic weakness, those spreads widen quickly.

Right now, they’re sitting near the lower end of their historical range.

Again, that is not what you’d normally expect to see if investors were genuinely worried about a major economic problem building underneath the surface.

None of this means markets can’t pull back. They can. They always can.

But when I look at these charts, I don’t see stress building. I don’t see fear spreading through credit markets.

And I don’t see the types of conditions that have typically existed before major bear markets.

What I see is a financial system that still looks healthy.

And that’s important because bull markets don’t usually die when financial conditions are calm. They usually die when stress starts spreading underneath the surface.

Right now, I’m struggling to find much evidence of that.

So if stress is not really showing up in the data, the next question becomes simple.

Where is the real opportunity?

When the Crowd Gets It Wrong

That’s why we spend so much time focused on human behavior at TrendLabs.

Indeed, at its core, The Divergence is built around a very simple idea.

We start by looking for crowded trades, such as stocks with heavy short interest, sectors where investors have become heavily positioned one way, and markets where large groups of people are effectively making the same bets.

Then we wait.

We’re not interested in fighting the crowd simply because a trade looks crowded.

A crowded trade can stay crowded for a long time.

What we’re looking for is evidence that something has started to change, like a shift in price behavior, or a signal that the trade may be starting to move against the people positioned on the wrong side of it.

That’s when things can get interesting.

Once a crowded trade starts moving the wrong way, the unwind can become powerful.

Short sellers become buyers. Investors who were underweight start chasing exposure. Money managers who were positioned for one outcome suddenly need to adjust.

What starts as a small move can quickly turn into something much larger.

That’s the opportunity we’re looking for.

Not the stock everyone is talking about, not the headline dominating social media, and not the story that already has everybody’s attention.

We’re looking for situations where positioning based on expectations and the reality of price start moving in different directions.

That’s where some of the best opportunities in markets tend to come from.

And that’s not all that different from the lesson I took away from the trip.

The biggest opportunity wasn’t an AI stock. It wasn’t the SpaceX IPO. It wasn’t a prediction about where the market goes next.

It was getting in a room with smart people, challenging ideas, testing theories, and improving the process.

Because the best opportunities usually aren’t obvious at the start.

If they were, everybody would already be there.

That’s why I spend so much time paying attention to the things most investors ignore.

Right now, those things continue to tell a different story from the one most investors seem focused on.

Investors sound stressed.

The market doesn’t.

Happy hitting🏌️⛳

Grant Hawkridge

Quantitative Analyst, TrendLabs