Founder’s Note: You can probably read the last three Saturday EWs from Grant Hawkridge – Data Beats Feel, The People Around You Shape Your Edge, and Why I Trust Charts– and come away with a good grasp of every major principle we talk about at TrendLabs.

But you should read this Saturday EW, too. And, also, stay tuned for more from Sam Gatlin next Saturday and Jason Perz the Saturday after that.

For now, though, here’s Grant with another great breakdown of concepts critical to everything we do… – JC

G’day, Grant here again.

When I was working through my Masters of Finance, “confirmation bias” came up a lot. The idea is simple: You form a view, and then you start looking for information that supports it.

At the time, it made sense. But it also felt like one of those things that happens to other people. Because when you’re actually in the market, it doesn’t feel like bias. It just feels like you’re seeing things clearly.

You build a view, you find reasons to support it, and you stick with it. There’s nothing in that process that forces you to step back and question it.

That part didn’t really click for me until I started spending time with JC and going through charts together.

You’d come in with a view, walk through the charts, and pretty quickly realize the market wasn’t confirming what you thought you were seeing.

Price has a way of doing that. It doesn’t confirm your opinion just because you believe it. It either shows up in price, or it doesn’t. When it doesn’t, that’s usually where you’re wrong.

Understanding confirmation bias is one thing, but seeing how it plays out in real time is something else entirely. The more time you spend looking at price, the more you realize that one signal on its own isn’t enough to trust.

In markets, confirmation isn’t about reinforcing your opinion. It’s about the market confirming the move.

Dow Theory, Updated for Today

The idea behind Dow Theory hasn’t changed. Markets don’t move on a single signal, they need confirmation. That was true a hundred years ago, and it’s still true today.

Back then, the idea was simple. Industrials represented production and Transports represented delivery. If the economy was strong, both had to be moving higher together.

It wasn’t enough for one to break out on its own. You needed the other to confirm it. That logic worked because it matched how the world operated at the time.

Goods were made, then they were shipped. If both sides of that equation were expanding, you had a healthy environment. If one started to lag, it usually meant something underneath the surface wasn’t lining up.

That foundation still holds, but the structure of the market has changed.

Dow Theory was never about those specific indexes. It was about tracking how the economy actually works.

A hundred years ago, that meant physical goods. Companies made things, and those goods had to be shipped. That’s why industrials and transports mattered.

But the economy doesn’t run that way anymore.

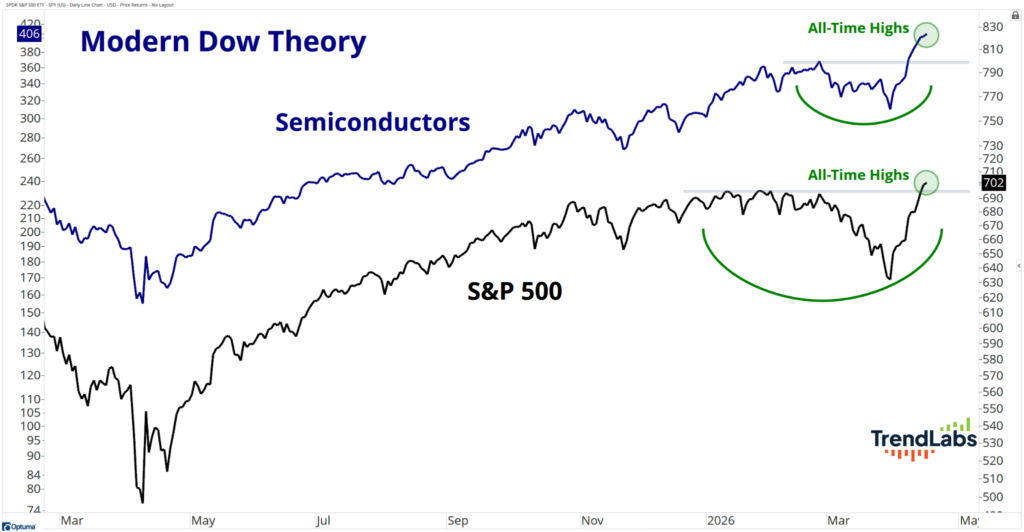

Today, you tend to see that strength show up in semiconductors. They sit at the center of how most businesses operate now. When companies are building and expanding, it shows up there.

But that move on its own isn’t enough.

The S&P 500 gives you the other side of it.

It’s not one theme or one group. It’s a broad mix of companies across the economy.

And while not every company makes chips, most companies rely on them to do business. Whether it’s software, logistics, payments, or manufacturing, it all runs on the same underlying technology.

So when strength starts to show up there as well, it tells you the move isn’t isolated. It’s spreading.

That doesn’t mean the original framework doesn’t matter. Industrials and transports still tell you something about the economy, and they’re still worth watching.

But the market has evolved, and so has the way we apply it.

We’re still looking for the same thing. One part of the market moves first, and another confirms it. We’re just using the parts of the market that reflect how the economy works today.

That’s how confirmation works. One part of the market can move first, but you need to see that strength show up elsewhere before you can trust it.

You can see that playing out clearly right now:

Semiconductors moved first. They pushed to new highs, pulled back in a controlled way, held their trend, and then turned higher again.

The S&P 500 followed. It went through its own pullback, built a base, and has now worked its way back up into fresh highs.

That’s the confirmation.

One move on its own doesn’t tell you much. It can stall, reverse, or just go nowhere.

But when you start to see that same strength show up in other parts of the market, that’s when it becomes something you can trust.

This is just a modern version of what Dow was doing all along. Back then it was industrials and transports. Today it’s semiconductors and the S&P 500.

Different inputs, same principle.

What Confirmation Tells Us To Do

Once the market confirms the move, the question changes. It’s no longer about whether the trend is higher, it’s about where to focus inside it.

That’s where we lean on the NOW Score.

We’re not trying to own everything. The focus is on the names already showing strength. The NOW Score ranks stocks based on trend, relative strength, and momentum working together.

Trend tells us if price is moving higher across timeframes and holding those levels. Relative strength shows us whether a stock is outperforming the rest of the market. Momentum tells us if that move is building.

When those three show up together, it usually means demand is there and money is flowing in early. In a market where strength has already been confirmed, that’s where the better opportunities tend to be.

But most people are still trying to figure out if it’s real confirmation or not.

We’re not guessing. We’re focusing on the names where that strength is already in place.

Happy hitting🏌️⛳

Grant Hawkridge

Quantitative Analyst, TrendLabs