I’m down here in Avalon, New Jersey, for the month of June, one of my favorite places in the world. Every year we pack up the family, move into a beach house, and spend the month by the ocean.

The kids spend all day on the beach. I work during the day with stock charts on one screen and the sound of seagulls outside the window.

This week my mother-in-law is visiting.

Anybody raising young kids knows how valuable that is. The kids love it. My wife loves it. Every now and then, we even get to sneak out for dinner or drinks by ourselves.

One evening I was checking the futures market as they opened up.

Stocks were rallying, and I found myself thinking out loud.

“Wow. Stocks are flying. I’m surprised the dollar isn’t down more.”

My mother-in-law immediately stopped me.

“What do you mean? Why would the dollar be down?”

It’s a great question.

She’s a successful businesswoman, but she doesn’t spend her days thinking about capital flows and intermarket relationships.

Her assumption was simple. If the dollar is stronger, isn’t that a good thing?

At first glance, that sounds perfectly reasonable.

For years we’ve been taught that a strong dollar means a strong economy, a strong country, and strong financial markets.

But that’s not usually how investors have treated it.

The Dollar’s Traditional Role

For most of my career, one of the easiest ways to think about the dollar was as a safe haven.

When investors got nervous, money flowed into dollars. When investors felt comfortable taking risk, money flowed into stocks, commodities, emerging markets, and other assets tied to economic growth.

That’s one reason the dollar’s weakness throughout much of 2025 never bothered me.

In fact, it made perfect sense.

The dollar peaked in late 2022, almost to the day stocks were putting in their bear market lows and preparing for a historic rally that’s still underway today.

As the dollar rolled over, stocks took off. Not just in the U.S., but around the world. That’s usually how these things go.

When investors get nervous, they rush into dollars. When fear fades, money starts moving elsewhere. Capital flows into stocks, commodities, international markets, and other assets that benefit when investors are willing to take risk.

By 2025, that’s exactly what we were seeing. Stocks were acting great. Credit was acting great. International stocks were acting great.

There was very little demand for safety because there was very little fear.

In that environment, a weaker dollar wasn’t surprising.

It was exactly what you’d expect.

Or was it?

Maybe we’ve been thinking about the relationship backwards.

Maybe stocks didn’t rally because the dollar was weak. Maybe the dollar was weak because stocks were rallying. Maybe investors simply had no reason to hide in cash when opportunities elsewhere were so attractive.

That’s where things start to get interesting.

Today, stocks remain near all-time highs, and participation continues to broaden across the market.

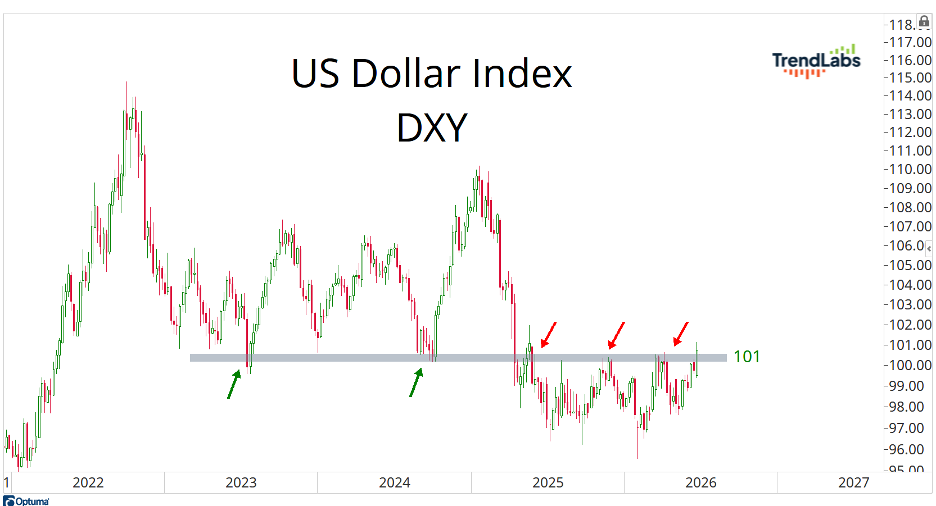

Investors are still favoring risk, yet the U.S. Dollar Index (DXY) just closed at a new 52-week high:

That’s not exactly how the script is supposed to read.

A New Regime?

One possibility is that the dollar is doing what it’s done many times throughout history.

Maybe it’s acting as an early warning signal.

Maybe money is starting to move toward safety before weakness in stocks becomes obvious to everyone else.

Markets are forward-looking, and some of the smartest investors in the world spend their lives trying to anticipate what’s coming next.

If that’s what’s happening, then a stronger dollar deserves our attention.

But there’s another possibility.

Maybe the dollar isn’t warning us about anything at all.

Maybe this move is simply a rally within a larger downtrend. Or maybe we’re entering an environment where both stocks and the dollar can thrive at the same time.

We’ve seen that movie before.

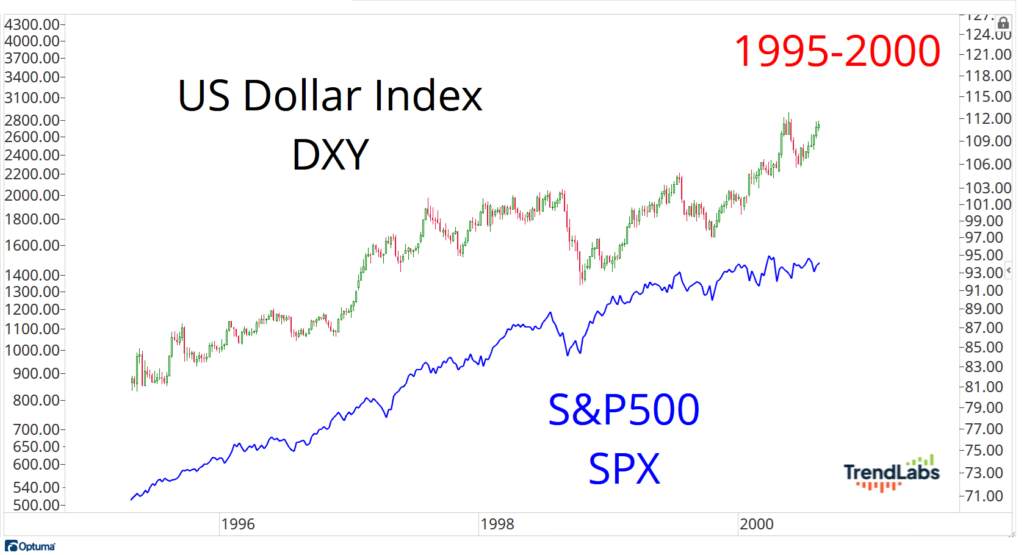

During the second half of the 1990s, investors around the world wanted exposure to American assets.

They wanted U.S. stocks. They wanted U.S. technology companies. They wanted dollars.

Capital poured into the United States, and stocks and the dollar benefited:

Could something similar be happening today?

It’s certainly possible.

A stronger dollar doesn’t always mean fear. Sometimes it means demand. Sometimes it means capital flowing toward opportunity. Sometimes it reflects confidence rather than caution.

I was discussing this recently with Chris Verrone, Chief Market Strategist at Strategas and one of the best in the business. I asked him whether the S&P 500 could rally toward 8,200 while the U.S. Dollar Index climbed to 105.

His response was simple. “Sure, why not?”

I threw the same question out on Twitter and got plenty of pushback.

That’s one of the things I love most about the community there. The best conversations aren’t the ones where everybody agrees. They’re the ones that force you to look at an idea from a different angle.

For most of my career, a stronger dollar and stronger stocks weren’t supposed to go together. Yet here we are with stocks near all-time highs, the rally broadening out across the market, and the U.S. Dollar Index closing at a new 52-week high.

That’s the question I’ve been thinking about lately.

One of the biggest misconceptions about technical analysis is that it’s supposed to provide all the answers. It doesn’t. What the best charts do is force us to ask questions we may not have considered otherwise.

Right now, the question is whether the dollar’s recent strength is a warning sign, a temporary detour, or evidence of a market environment that looks very different from the one investors have grown accustomed to.

Because if the dollar continues strengthening while stocks continue climbing, it won’t just challenge a popular market relationship.

It will challenge one of the most widely accepted assumptions investors have held for decades.

Stay sharp,

JC Parets, CMT

Founder, TrendLabs