I found myself standing underneath the Space Shuttle Enterprise on Sunday with my twin three-year-old boys asking me questions about rockets, planets, and astronauts.

Pretty awesome way to spend an afternoon.

I lived in New York City for more than a decade and somehow never made it to the Intrepid. Which is crazy because I probably drove past that aircraft carrier a thousand times without thinking twice about it.

This weekend we brought the kids into the city for a few days. Broadway show. Central Park. Pizza. New York stuff.

By Sunday, the girls had their own plans. So me and the boys went full jets-and-rockets mode.

And while they were busy throwing toy planets at each other and climbing all over fighter jets, I couldn’t help but laugh at the irony of what’s happening in the market right now. Specifically this massive rumored $2 trillion SpaceX IPO everybody suddenly can’t stop talking about.

Because the timing here is fascinating.

Historically, these giant IPO waves tend to show up much later in the cycle than earlier.

Venture capital firms and early investors usually aren’t racing to sell shares to the public when conditions are uncertain. They do it when demand is overwhelming and investors are feeling invincible.

In other words, they sell when people are excited to buy.

At the same time, some of the market signals I trust most are starting to flash warnings beneath the surface even while the S&P 500 keeps pushing to new highs.

That combination caught my attention.

And on the drive home, with the boys asleep in the backseat after a full day of rockets and fighter jets, I found myself thinking about risk appetite, defensive positioning and whether this latest IPO frenzy is showing up at a very inconvenient time for investors chasing the story.

The Fun Stuff vs The Boring Stuff

One of the biggest mistakes investors make is assuming all new highs are created equal.

They’re not.

Sometimes markets are healthy underneath the surface. Money flows into aggressive areas. Investors are willing to take risk. Participation expands. Cyclical groups lead the way.

Other times, the indexes keep drifting higher while investors quietly start hiding in more defensive areas behind the scenes.

That’s the environment I think we’re moving into now.

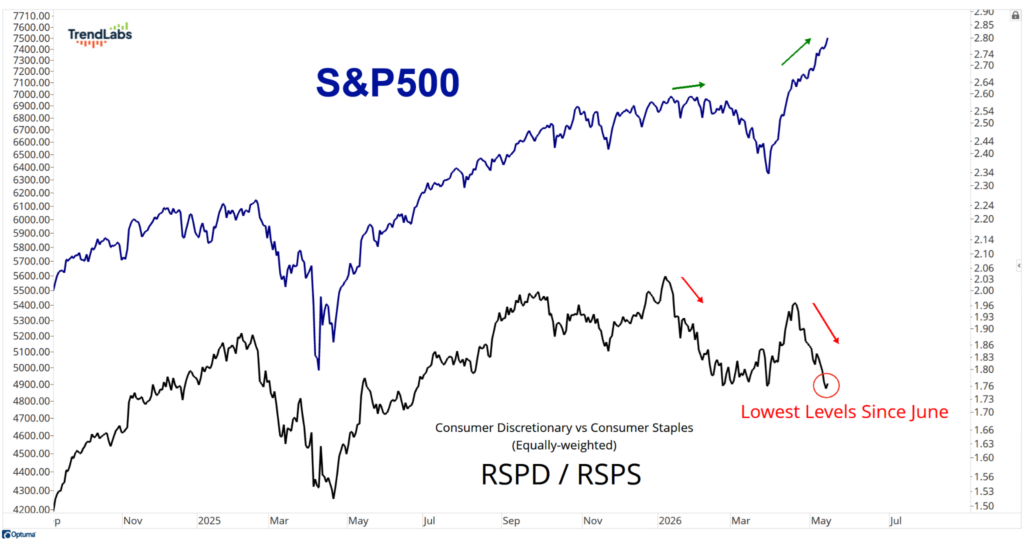

There’s a ratio I watch constantly that compares consumer discretionary stocks against consumer staples. In plain English, it measures whether investors want to own the fun stuff or the boring stuff.

Do they want homebuilders, retailers, and automobiles?

Or do they want toothpaste, laundry detergent, and canned soup?

A lot of us regularly call this ratio the “greatest fundamental analyst on Wall Street,” which honestly cracks me up every time I hear it because it’s literally just price behavior telling us how investors are positioning.

Lately, investors are getting a lot more defensive.

Even with the S&P 500 pushing to fresh all-time highs this week, this ratio just hit its lowest level since last summer:

That’s not the type of behavior you normally see during the healthiest parts of a bull market.

This is exactly why I couldn’t stop thinking about the SpaceX IPO while standing underneath that Space Shuttle.

The surface-level story sounds incredible. AI. Space. Rockets. Innovation. Trillion-dollar valuation. Everybody wants in.

But underneath the surface, investors are already starting to rotate toward defense.

That disconnect is hard to ignore.

We Live in a Market-Cap Weighted World

Now here’s where it gets even more interesting.

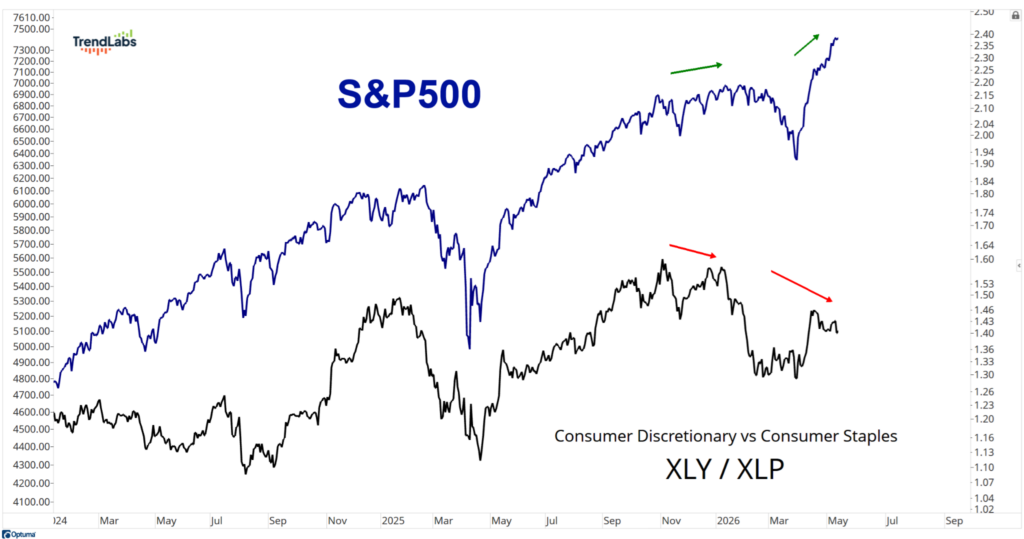

Equal-weight ratios are useful because they show us what the average stock is doing. But the reality is markets are driven by the biggest companies on earth.

The generals matter.

So we also want to know whether the largest consumer discretionary stocks are keeping up with the largest consumer staples stocks.

And they’re not.

In fact, we’re seeing the exact same defensive rotation happening there, too:

This is the type of stuff most investors never see because everybody’s too busy staring at the S&P 500 headline number on television.

“Market hits new highs” sounds great.

But underneath the hood, fund managers are slowly reaching for the airbags instead of the accelerator.

And there’s another layer to this that makes the timing even harder to ignore.

Last year, we flagged something we call “The Omen,” a rare breadth thrust signal that historically marked the beginning of one of the strongest 12-month windows investors ever get.

That window expired last week.

For the past year, stocks had an enormous tailwind behind them. Breadth was expanding. Participation was broadening out. Breakouts were working everywhere.

Historically, those are the periods where investors want to be aggressive because the market is effectively doing a lot of the heavy lifting for you.

Now that backdrop is gone.

That doesn’t mean the bull market is dead. It simply means the market no longer has the same historical cushion underneath it that existed over the past 12 months.

And it’s happening right as some of the biggest IPOs in the world are being handed over to public investors.

That’s a very different environment than the one we were operating in a year ago.

That doesn’t automatically mean disaster is coming tomorrow morning.

Markets are messy. Trends evolve. Rotations happen.

But it absolutely changes the type of environment we’re operating in. And if the environment changes, then the playbook has to change, too.

That’s the game.

As I sat there listening to retired astronauts talk about space exploration while my boys launched stuffed planets at each other, I couldn’t help but laugh at how perfectly timed this all feels.

The biggest space IPO in history might be arriving right as investors are quietly becoming less interested in taking risk.

That’s not a sign this story will end well for the public.

The afternoon with the boys was a huge success.

My suspicion is the IPO cycle won’t be.

Stay sharp,

JC Parets, CMT

Founder, TrendLabs