I spend a lot of time looking at charts every week.

After doing this for more than two decades, I’ve learned which ones deserve a closer look.

Most of them just blend together after a while. Some look constructive. Some look terrible. Some are just noise dressed up as conviction from people trying to sound smarter than they are.

Every now and then, though, you run into one chart that makes you stop scrolling. But not because it confirms your opinion.

The dangerous charts are usually the ones that challenge it. Right now, one chart keeps jumping off the screen at me.

What makes it interesting is that it’s not some obscure indicator from a PhD thesis nobody understands.

This is about one of the most important groups in the entire global stock market. The kind of companies everybody recognizes. The kind of businesses sitting right in the middle of the economy.

Banks.

And what they’re doing relative to the rest of the stock market is something we’ve literally never seen before.

Now, before everybody starts running around screaming recession, collapse, crisis, financial contagion, or whatever scary word gets the most clicks this week, let’s slow down for a second.

Because markets are rarely that simple.

One of the biggest mistakes investors make is treating every chart like it exists in isolation. It doesn’t.

You have to weigh the evidence. You have to look at trends, participation, leadership, relative strength, absolute strength, sentiment, positioning, all of it together.

That’s the game.

Although this particular chart is definitely waving a giant yellow caution flag, there’s another side to the story that the bears probably aren’t going to like very much.

So let’s walk through it.

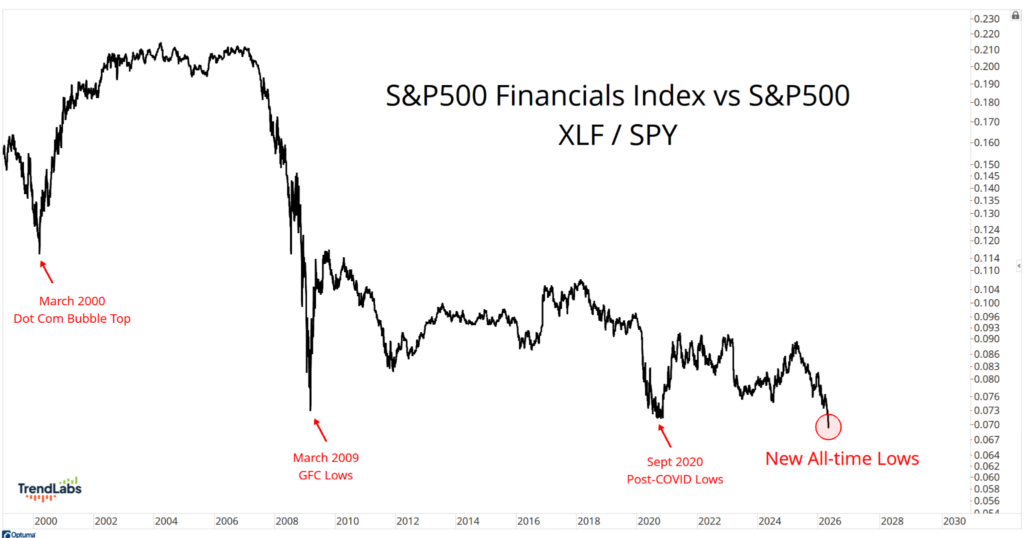

New All-Time Lows for Financials Relative Strength

There’s one thing we keep seeing over and over again across global markets:

The indexes with more technology exposure keep outperforming the ones with less.

And nowhere is that showing up more clearly than in financials.

On Monday, the S&P 500 Financials ETF (XLF) closed at the lowest levels in history relative to the S&P 500 itself:

Think about what that means for a second.

Some of the biggest and most important financial institutions in the world – names like JPMorgan Chase (JPM), Goldman Sachs (GS), Visa (V), Mastercard (MA), Morgan Stanley (MS), and Bank of America (BAC – are underperforming the broader stock market more than they ever have before.

These new lows even undercut the depths of the 2008-09 Great Financial Crisis and the COVID-19 panic lows.

That definitely gets my attention.

Because historically, healthy bull markets usually have participation from financials. Banks sit at the center of the economy. Credit drives everything.

So when a sector this important starts lagging to this degree, you can’t just ignore it and pretend it’s meaningless.

But here’s the key: Relative weakness and absolute weakness are not the same thing.

And that distinction is probably the entire ballgame right now.

No Tech vs A Lot of Tech

When you zoom out, this Financials ratio is really telling the same story we’re seeing all over the world.

The more technology exposure an index has, the better it’s been performing.

Countries like South Korea, Taiwan, and Israel – markets heavily tied to technology and semiconductors – continue to crush countries dominated by things like natural resources and old economy sectors.

Growth stocks are outperforming value. High beta is outperforming low volatility.

Aggressive leadership keeps beating defensive positioning.

And a lot of that comes down to one thing: tech.

Financials don’t have any technology stocks in their sector index, by definition. The S&P500, meanwhile, is now pushing toward a 36% weighting in Technology alone.

So part of this historic underperformance from Financials isn’t necessarily because banks are collapsing.

It’s because they’re competing against the strongest secular trend in the market during the middle of an AI arms race.

That’s a very different conversation.

Because there’s a huge difference between “financials are weak” and “technology is unstoppable.”

Right now, the evidence points much more toward the second one.

What About the Absolute Trend?

Here’s where things get interesting.

Yes, financials are getting smoked on a relative basis by technology.

There’s no debating that.

But relative underperformance alone doesn’t automatically mean we’re dealing with some massive bear market about to rip everyone’s face off.

Because while banks are lagging the S&P500, the actual bank stocks themselves are still doing just fine.

In fact, the S&P Bank ETF (KBE) just closed April at new all-time highs:

Honestly, that’s a really hard thing for the bears to explain away.

If the banking system were truly cracking beneath the surface, you probably wouldn’t see bank stocks making fresh highs.

You’d see failed breakouts. You’d likely see expanding credit stress. You’d definitely start to see aggressive selling.

Instead, what we have is a banking sector that simply can’t keep up with the strongest technology leadership environment of our lifetime.

Those are very different things.

Could this relative breakdown in financials eventually turn into something bigger?

Of course. Markets are always changing. We stay open-minded. We keep weighing the evidence.

But if you’re building the case for a major stock market collapse, I think you need the banks to participate on the downside.

So far, they’re not doing that. Actually, they’re doing the opposite.

The most bearish chart in the world still hasn’t broken the bull market.

At least not yet.

Stay sharp,

JC Parets, CMT

Founder, TrendLabs